Comprehensive and collision are often bundled together, but they trigger in completely different scenarios — and one costs 62% more than the other. Here's how to decide if you need both, one, or neither.

The Core Difference: What Triggers Each Coverage

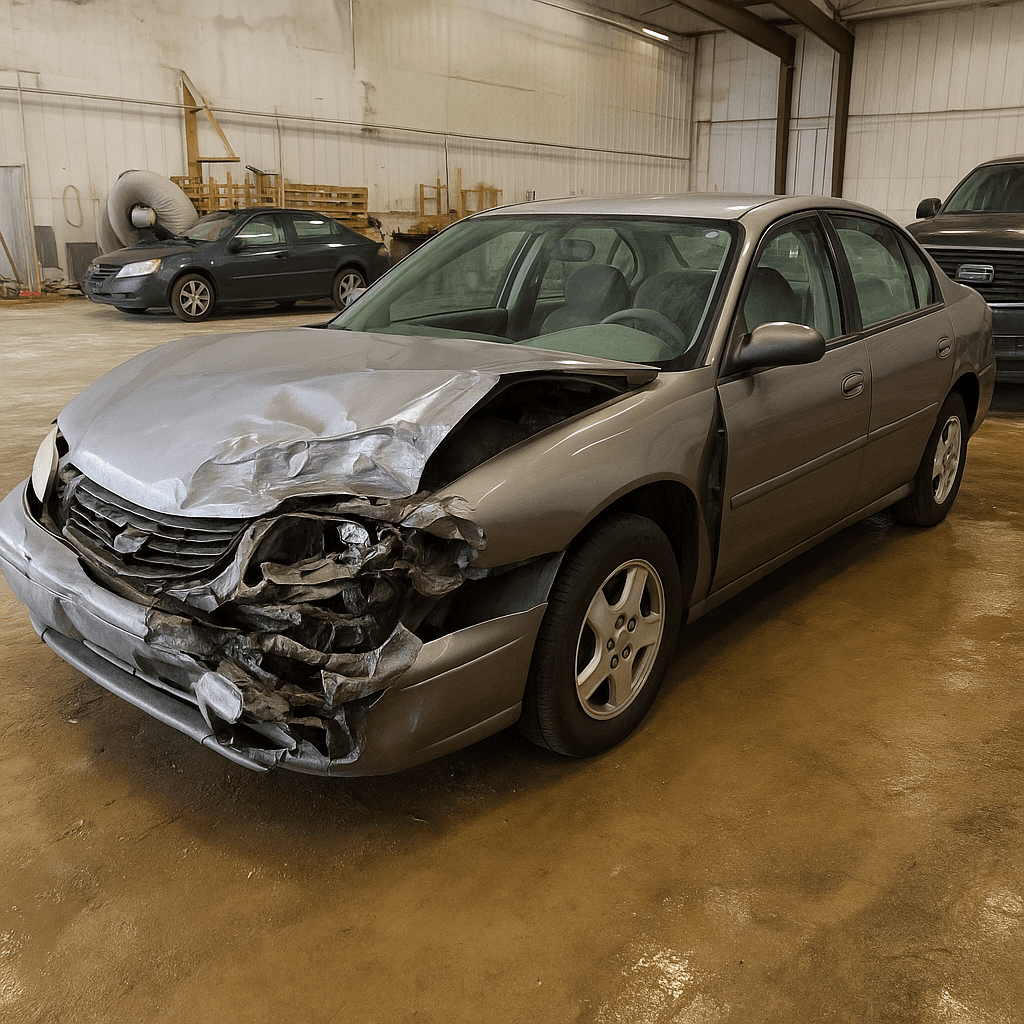

Collision coverage pays when your vehicle hits another object or flips over. The object can be another car, a guardrail, a tree, or a mailbox. If your car was moving and made contact with something, collision handles the repair bill.

Comprehensive coverage pays for nearly everything else that damages your vehicle while it's parked or in motion. This includes theft, vandalism, hail, flooding, fire, animal strikes, falling tree limbs, and windshield cracks. The common thread: no collision with another vehicle or fixed object while driving.

The confusion comes from bundling. Most lenders require both coverages if you finance or lease a vehicle, so drivers rarely choose just one. But they're sold separately, priced differently, and apply to completely different loss scenarios.

National Cost Data: Collision Runs 62% Higher on Average

According to National Association of Insurance Commissioners data, the average annual cost for collision coverage in the U.S. is approximately $381, while comprehensive averages $235. That means collision costs roughly 62% more than comprehensive for the same vehicle and driver profile.

The pricing gap reflects claim frequency and severity. Collision claims are more common — drivers hit objects far more often than they experience theft or hail damage. Collision repairs also tend to be expensive: a front-end collision can easily exceed $8,000 in repair costs on a modern vehicle with sensors and cameras embedded in bumpers.

Comprehensive claims, while less frequent, can still be severe. Total theft of a financed $35,000 SUV triggers a comprehensive claim that pays out the actual cash value. But statistically, comprehensive claims happen less often and average lower payouts, which is why premiums are lower.

Compare auto insurance rates in your state

Get matched with licensed carriers in minutes. One short form, real quotes, no obligation.

Get Your Free Quote✓ Free to Compare✓ No Obligation✓ Licensed Carriers✓ TCPA Compliant

When You Need Both, One, or Neither

If you're financing or leasing a vehicle, your lender will require both coverages until the loan is paid off. This is non-negotiable. The lender has a financial interest in the vehicle and won't accept the risk of you totaling it without insurance covering the replacement cost.

If you own your car outright, the decision depends on vehicle value and your financial cushion. A common rule of thumb: if your car is worth less than $4,000 and you have savings to replace it, dropping both coverages can save $600–$800 per year. If your car is worth $12,000 or more, keeping both is usually prudent unless you can absorb a total loss without financial strain.

Some drivers drop collision but keep comprehensive on older vehicles, especially in areas with high rates of theft, hail, or deer strikes. Comprehensive is cheaper and covers risks you can't control through defensive driving. Collision, meanwhile, protects against at-fault accidents — a risk some experienced drivers with older cars are willing to self-insure.

Deductible Strategy: How It Affects Your Premium and Out-of-Pocket Cost

Both comprehensive and collision require you to choose a deductible — the amount you pay before insurance covers the rest. Standard deductible options are $250, $500, $1,000, and sometimes $2,000. Raising your deductible from $500 to $1,000 typically reduces your premium by 15–30%, depending on the insurer and state.

Choosing a higher deductible makes sense if you have emergency savings and want lower monthly premiums. A driver paying $45/month for collision with a $500 deductible might drop to $35/month with a $1,000 deductible — saving $120/year. But if you file a claim, you'll pay an extra $500 out of pocket.

You can set different deductibles for comprehensive and collision. Some drivers choose a lower comprehensive deductible (e.g., $250) because comprehensive claims are often smaller — a cracked windshield might cost $400 to replace — and a higher collision deductible (e.g., $1,000) to save on the more expensive premium.

Real Scenarios: Which Coverage Applies

A deer runs into the side of your car while you're driving on a rural highway. Comprehensive pays, because an animal strike is not a collision with a vehicle or fixed object.

You swerve to avoid the deer and hit a guardrail. Collision pays, because you struck a fixed object. Even though the deer caused the swerve, the actual damage came from hitting the guardrail.

Your car is stolen from your driveway. Comprehensive pays. If the thief crashes your car into a pole and it's later recovered, comprehensive still handles it — theft and vandalism fall under comprehensive even if the thief causes collision damage.

You back into a concrete pillar in a parking garage. Collision pays, because you hit a stationary object.

A hailstorm dents your hood and roof while the car is parked. Comprehensive pays. Weather-related damage is never a collision claim.

How Claims Affect Future Premiums Differently

Filing an at-fault collision claim typically raises your premium more than filing a comprehensive claim. Industry data suggests at-fault collision claims increase premiums by 20–40% at renewal, depending on the carrier and your claims history. Comprehensive claims generally result in smaller increases — often 10–20% — because they're considered not-at-fault events.

Some insurers offer accident forgiveness, which prevents your first at-fault accident from raising your rate. This applies to collision claims. Comprehensive claims are less likely to trigger forgiveness programs, but they also trigger smaller surcharges to begin with.

If your comprehensive claim is below a certain threshold — often around $1,000–$1,500 — some carriers won't surcharge you at all. A $600 windshield replacement might not affect your rate. But a $600 fender bender from backing into a mailbox could still raise your premium, because it signals at-fault driving behavior.

Should You Drop Coverage on an Older Car?

The break-even analysis is straightforward. If you're paying $50/month for both coverages combined ($600/year) and your car is worth $3,500, you'll recover your annual premium after six years of no claims — at which point your car will be worth even less. In this scenario, self-insuring makes financial sense if you can cover a $3,500 loss.

But consider your specific risks. If you live in a high-theft ZIP code or an area prone to hail, keeping comprehensive for $20/month might be worth it even on a $4,000 car. Theft and total-loss hail claims don't require fault, and comprehensive premiums stay low even on older vehicles.

If you drop coverage and later want to add it back, insurers will allow it — but if your car depreciates significantly or sustains prior damage, you may get less payout than you expected. Once you drop coverage, you're accepting the vehicle's condition and value risk from that point forward. compare quotes