Most drivers treat state minimums as a yes/no question, but the real decision is whether you can afford what minimums don't cover after an at-fault crash.

The Real Question Isn't Coverage — It's Your Exposure After a Crash

You're staring at two premium quotes: one for state minimum coverage at $45/mo, another for 100/300/100 limits at $87/mo. The difference feels significant when you're on a tight budget. But the question isn't whether minimum coverage meets legal requirements — it does. The question is whether you can personally afford the financial gap if you cause a crash that exceeds those limits.

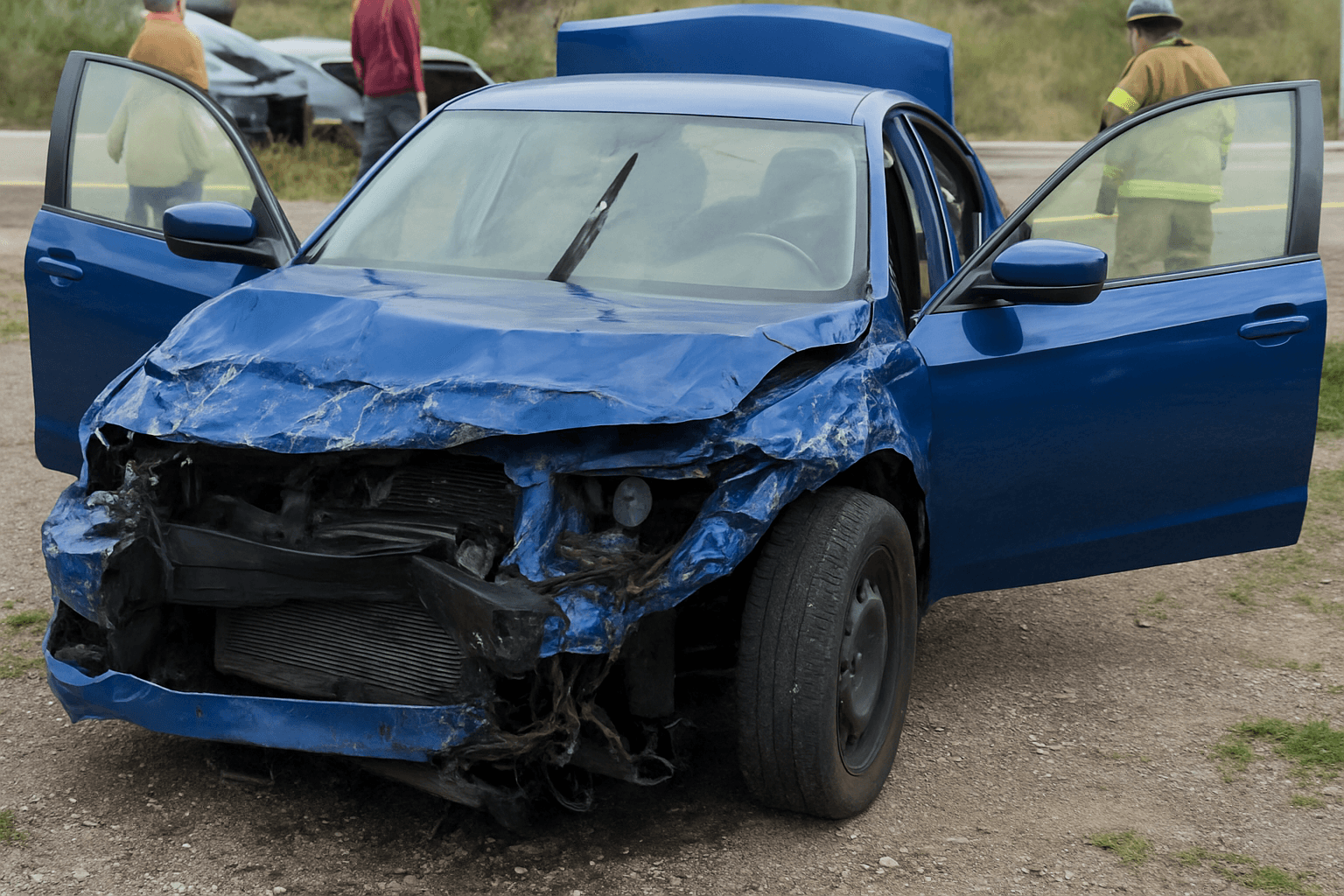

Most states require liability minimums between 25/50/25 and 30/60/25, meaning $25,000–$30,000 per person for injuries, double that per accident, and $25,000 for property damage. The average injury claim from a moderate-severity crash runs approximately $40,000–$60,000, and a totaled newer SUV can easily exceed $35,000. If your policy caps at $25,000 and the injured party sues for $60,000, you're personally liable for the $35,000 difference.

State minimums work for exactly one scenario: you have minimal assets, earn close to median income or below, and could feasibly settle a lawsuit through a payment plan or discharge the debt without catastrophic loss. If you own a home with equity, hold retirement accounts above your state's exemption limits, or earn above-median wages that can be garnished, minimum coverage shifts significant risk onto your balance sheet. liability insurance uninsured motorist coverage

Where State Minimums Fall Short — By the Numbers

California requires 15/30/5 liability limits. That $5,000 property damage ceiling doesn't cover a totaled Honda Accord, which averages around $27,000 new. If you rear-end one at a stoplight, your insurer pays the first $5,000. You're sued for the remaining $22,000. Florida's 10/20/10 minimums are even lower — property damage caps at $10,000, while the average vehicle on the road is valued near $28,000 according to Kelley Blue Book data.

Medical costs create larger exposure. The average ER visit for a crash-related injury runs $3,000–$10,000 depending on severity, and that's before imaging, surgery, or follow-up care. A broken bone with surgery can reach $30,000–$50,000. If your per-person limit is $25,000 and the injured driver incurs $45,000 in medical bills, you owe the difference personally. Multiply that by two injured occupants and you're facing $40,000 in personal liability even on a relatively common two-car intersection collision.

Property damage limits also fail to account for commercial vehicles. A loaded contractor van with tools and equipment can exceed $60,000 in value. A small business delivery truck can run $80,000. Your $25,000 property damage limit covers less than a third of the loss, and business owners are far more likely to pursue legal recovery than individual drivers.

Compare auto insurance rates in your state

Get matched with licensed carriers in minutes. One short form, real quotes, no obligation.

Get Your Free Quote✓ Free to Compare✓ No Obligation✓ Licensed Carriers✓ TCPA Compliant

When Minimums Are Actually Enough — The Financial Threshold

State minimums make sense if you meet all three conditions: limited assets, income near or below the median for your state, and no major equity in property or retirement accounts. If your net worth sits below $15,000–$20,000 and your income falls under garnishment protection thresholds in your state, a judgment creditor has little to pursue even if you lose a lawsuit.

Many states exempt wages up to a certain multiple of the federal poverty line or minimum wage from garnishment. If you're judgment-proof due to income and asset limits, paying for coverage beyond minimums may not reduce your actual financial risk. The injured party can win a judgment, but if you have nothing to collect, the practical exposure is limited.

This calculus changes the moment you have attachable assets. Homeownership is the clearest threshold. If you own property with $40,000 in equity, a $35,000 judgment puts that equity at risk. Retirement accounts above your state's exemption cap — often $50,000–$100,000 depending on state law — are similarly vulnerable. If you're building wealth or own property, state minimums transfer crash risk from your insurance policy to your personal balance sheet.

The Cost Gap Between Minimum and Adequate Liability Coverage

Upgrading from state minimums to 100/300/100 liability limits typically adds $30–$60/mo depending on your driving record, age, and state. That's $360–$720 annually. Over a ten-year period with no at-fault crashes, you'll pay $3,600–$7,200 more for higher limits. If you cause one crash that exceeds minimum limits by $40,000, you break even in the first incident.

The premium difference shrinks significantly if you're already paying for comprehensive and collision coverage on a financed vehicle. Liability upgrades are calculated as a percentage of base risk, and if your total premium is already $140/mo with full coverage, jumping to 100/300/100 might add only $25–$35/mo. The marginal cost of better liability protection decreases as your overall coverage increases.

Some insurers offer 50/100/50 as a middle-tier option, typically priced $15–$30/mo above state minimums. This doubles your per-person injury coverage and quadruples property damage limits in low-minimum states, closing the most common exposure gaps without jumping to the highest available limits. For drivers with moderate assets — a car worth $12,000, $20,000 in savings, renting rather than owning — this middle tier often represents the break-even point between premium cost and realistic lawsuit risk.

What Minimums Never Cover — And Why That Matters Now

State minimum liability policies don't include collision or comprehensive coverage, meaning damage to your own vehicle comes out of pocket regardless of fault if you're in a single-vehicle crash or hit by an uninsured driver. If your car is worth $8,000 and you total it hitting a deer, you're walking unless you have comprehensive coverage. Collision coverage pays for at-fault crashes where you damage your own vehicle — minimums leave you with the repair bill and no car.

Uninsured and underinsured motorist coverage is optional in most states, and minimum-premium policies rarely include it unless required by state law. Approximately 13% of drivers nationally are uninsured according to the Insurance Information Institute, and many more carry only state minimums themselves. If an uninsured driver totals your car and injures you, your minimum liability policy pays nothing for your losses. You're left suing an uninsured defendant, which statistically recovers little.

Medical payments coverage and personal injury protection are similarly absent from bare-minimum policies in states where they're optional. If you're injured in a crash you cause, your liability policy pays the other driver's medical bills but not your own. You're reliant on health insurance, which may not cover all crash-related costs and often involves higher deductibles than PIP or MedPay would carry.

How to Decide If Minimums Work for Your Situation

Run a simple asset test: add up the value of your car, savings, home equity if you own property, and retirement accounts above your state's exemption limits. If that total exceeds $25,000–$30,000, you have attachable assets that a judgment creditor can pursue. Compare that figure to your state's minimum liability limits. The gap is your personal exposure.

Next, calculate the premium difference between minimums and 50/100/50 or 100/300/100 limits from at least three insurers. If the annual cost difference is less than 5% of your attachable assets, higher limits are mathematically defensible. A $500/year increase to protect $40,000 in home equity represents a 1.25% annual insurance cost on that asset — far cheaper than the risk of losing it in a lawsuit.

Consider your driving exposure separately from your asset position. If you drive fewer than 5,000 miles annually in low-traffic rural areas, your crash probability is materially lower than someone commuting 40 miles daily in dense metro traffic. Lower exposure can justify accepting more risk through minimum coverage, but only if your asset position also supports it. High-mileage drivers with attachable assets should rarely carry minimums regardless of premium sensitivity. compare quotes